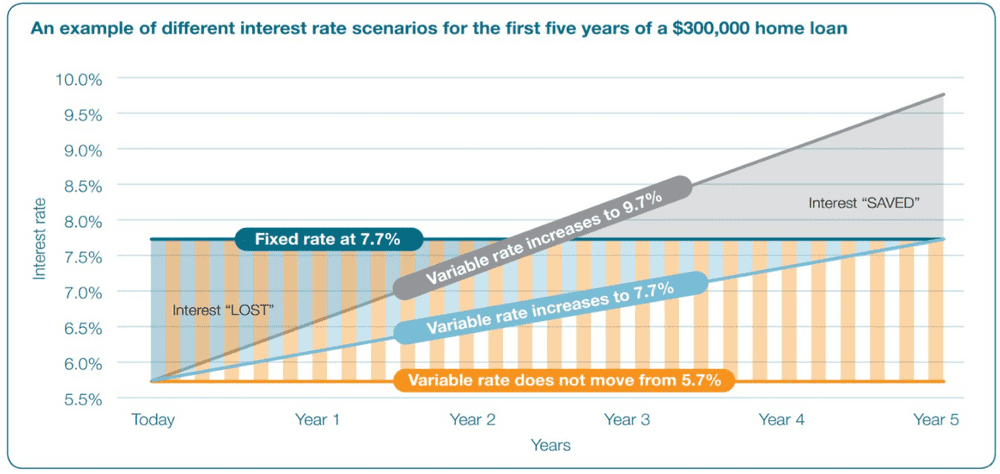

Rate locks can be found in numerous types a percentage of your mortgage quantity, a flat one-time cost, or merely an amount figured into your rate of interest. You can lock in a rate when you see one you desire when you first apply for the loan or later on at the same time. While rate locks usually avoid your interest rate from increasing, they can likewise keep it from decreasing.

A rate lock is worthwhile if an unexpected increase in the rate of interest will put your mortgage out of reach - how do mortgages work in monopoly. If your down payment on the purchase of a house is less than 20 percent, then a lender might require you to pay for personal home loan insurance coverage, or PMI, because it is accepting a lower amount of up-front money toward the purchase.

The cost of PMI is based upon the size of the loan you are looking for, your down payment and your credit history. For instance, if you put down 5 percent to buy a home, PMI might cover the extra 15 percent. If you stop making payments on your loan, the PMI activates the policy payment in addition to foreclosure proceedings, so that the loan provider can repossess the house and offer it in an attempt to regain the balance of what is owed.

Your PMI can also end if you reach the midpoint of your reward for instance, if you secure a 30-year loan and you total 15 years of payments.

Considering getting a 30-year fixed-rate home loan? Good concept. This granddaddy of all home loans is the option of nine out of every 10 home buyers. It's no mystery why 30-year fixed-rate mortgages are so popular. Since the payment duration is long, the month-to-month payments are low. Due to the fact that the rate is fixed, homeowners can count on month-to-month payments that stay the very same, no matter what although taxes and insurance coverage premiums may alter.

A 30-year mortgage is a house loan that will be settled totally in 30 years if you make every payment as arranged. A lot of 30-year mortgages have a set rate, indicating that jasmine ekberg the interest rate and the payments remain the very same for as long as you keep the home loan. Lower payment: A 30-year term allows a more inexpensive month-to-month payment by extending the payment of the loan over a long periodFlexibility: You can pay off the loan quicker by contributing to your monthly payment or making additional payments, however you can constantly draw on the smaller sized payment as required "A 30-year home mortgage is a house loan that will be settled completely in thirty years if you make every payment as arranged.

The 7-Minute Rule for How Do Canadian Mortgages Work

In the early years of a loan, most of your home loan payments approach paying off interest, producing a meaty tax deduction. Simpler to certify: With smaller sized payments, more customers are qualified to get a 30-year mortgageLets you fund other goals: After home loan payments are made monthly, there's more cash left for other goalsHigher rates: Because lenders' danger of not getting repaid is spread out over a longer time, they charge higher interest ratesMore interest paid: Paying interest for thirty years amounts to a much greater total expense compared with a much shorter loanSlow growth in equity: It takes longer to construct an equity share in a homeDanger of overborrowing: Receiving a bigger home mortgage can lure some people to get a larger, better house that's more difficult to pay for.

Greater upkeep costs: If you opt for a more expensive home, you'll face steeper expenses for real estate tax, maintenance and perhaps even utility costs. "A $100,000 house might require $2,000 in annual upkeep while a $600,000 house would require $12,000 per year," says Adam Funk, a qualified financial planner in Troy, Michigan.

With a little preparation, you can integrate the safety of a 30-year home loan with among the main advantages of a much shorter home loan a much faster path to totally owning a home. How is that possible? Settle the loan faster. It's that simple. If you want to attempt it, ask your lender for an amortization schedule, which reveals how much you would pay monthly in order to own the home entirely in 15 years, twenty years or another timeline of your choosing.

Making your home loan payment immediately from your savings account lets you increase your month-to-month auto-payment to fulfill your objective but bypass the boost if required. This method isn't similar to a getting a much shorter mortgage because the interest rate on your 30-year mortgage will be a little higher. Rather of 3.08% for a 15-year set https://karanaujlamusiczpb1c.wixsite.com/landendwzz559/post/h1-styleclearboth-idcontentsection0the-smart-trick-of-how-do-reverse-mortgages-work-with-nursing-hom mortgage, for example, a 30-year term might have a rate of 3.78%.

For home mortgage shoppers who want a shorter term however like the flexibility of a 30-year home loan, here's some recommendations from James D. Kinney, a CFP in New Jersey. He suggests buyers evaluate the regular monthly payment they can pay for to make based upon a 15-year home loan schedule but then getting the 30-year loan.

Whichever method you pay off your house, the most significant advantage of a 30-year fixed-rate home loan might be what Funk calls "the sleep-well-at-night effect." It's the assurance that, whatever else alters, your house payment will remain the exact same.

Examine This Report on How Do Fha Va Conventional Loans Abd Mortgages Work

Purchasing a house with a home mortgage is most likely the largest monetary deal you will enter into. Usually, a bank or home loan lending institution will fund 80% of the price of the house, and you accept pay it backwith interestover a particular duration. As you are comparing lending institutions, mortgage rates and options, it's helpful to comprehend how interest accumulates each month and is paid.

These loans featured either repaired or variable/adjustable rate of interest. Most home mortgages are completely amortized loans, implying that each regular monthly payment will be the same, and the ratio of interest to principal will change gradually. Put simply, every month you pay back a part of the principal (the amount you have actually borrowed) plus the interest accrued for the month.

The length, or life, of your loan, also identifies how much you'll pay every month. Totally amortizing payment refers to a routine loan payment where, if the debtor pays according to the loan's amortization schedule, the loan is totally paid off by the end of its set term. If the loan is a fixed-rate loan, each completely amortizing payment is an equal dollar quantity.

Extending payments over more years (as much as 30) will normally result in lower regular monthly payments. The longer you require to settle your home mortgage, the higher the general purchase expense for your house will be due to the fact that you'll be paying interest for a longer duration. Banks and lenders primarily provide two types of loans: Rate of interest does not change.

Here's how these work in a home mortgage. The regular monthly payment stays the exact same for the life of this loan. The rates of interest is secured and does not alter. Loans have a payment life period of 30 years; much shorter lengths of 10, 15 or twenty years are likewise typically readily available.